- Muni bonds may offer security and tax-free portfolio income with relatively low default risk.

- These assets typically pay off for investors in higher tax brackets versus lower-income retirees.

- However, it can be tricky to manage individual muni bonds due to interest rate and credit risks, financial experts say.

If you're looking for a relatively safe, tax-friendly asset, you may be eyeing municipal bonds, known as muni bonds or "munis."

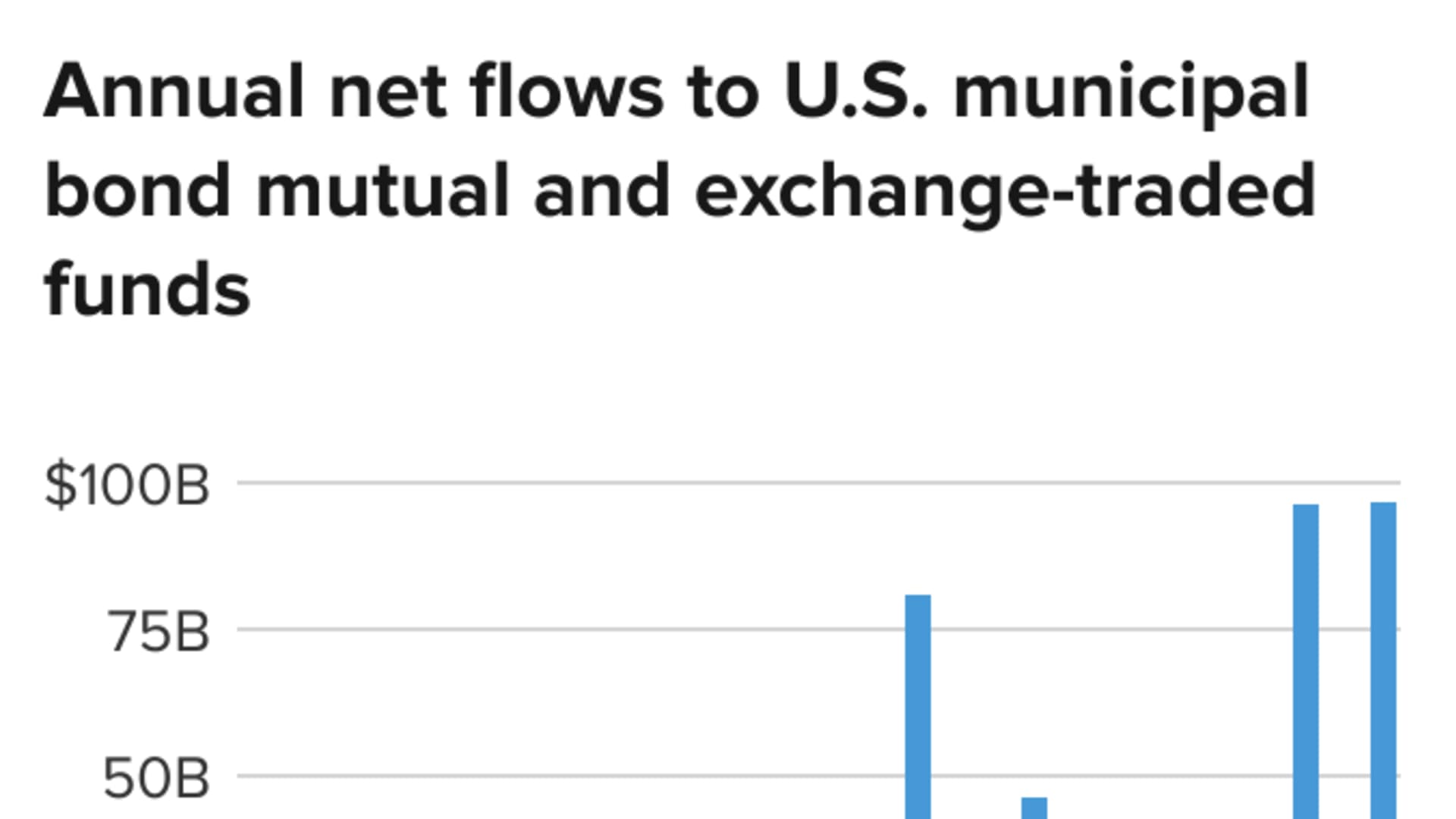

Demand soared in 2021 as investors fled from President Joe Biden's proposed tax increases, with a record $96.8 billion of net money pouring into U.S. muni mutual and exchange-traded funds, according to Refinitiv Lipper data.

Since rising market interest rates typically cause bond prices to fall, some investors worry about the Federal Reserve's expected interest rate hikes. But muni bonds are still a good option for certain clients, advisors say.

Get top local stories in Southern California delivered to you every morning. >Sign up for NBC LA's News Headlines newsletter.

More from Fixed Income Strategies:

Here's how rising interest rates may affect your bond portfolio in retirement

How new life expectancy tables affect required withdrawals from IRAs, 401(k) plans

'We are in a very precarious position.' How bond ladders can help fight rising interest rates

One of the primary benefits of muni bonds is safety.

"I like muni bonds as a place for clients to park their money," said certified financial planner Jordan Benold, partner at Benold Financial Planning in Prosper, Texas, explaining how it's a good spot for funds awaiting other opportunities.

Indeed, muni bonds tend to be less risky than their corporate counterparts, with 113 muni bond defaults out of 13,140 issuers from 1970 to 2019, according to Moody's, a bond rating company.

Money Report

The other draw is you can generally avoid federal taxes on interest and may skip state and local levies, depending on where you live.

For example, higher earners in California may save more than retirees in Tennessee, an income-tax-free state.

However, the lower your income, the less of a tax benefit you'll receive, said Seth Mullikin, a CFP and financial advisor at Lattice Financial, LLC in Charlotte, North Carolina.

"Munis don't make sense for a lot of clients in lower tax brackets because they aren't saving that much," he said. "And they're stuck with a lower yield."

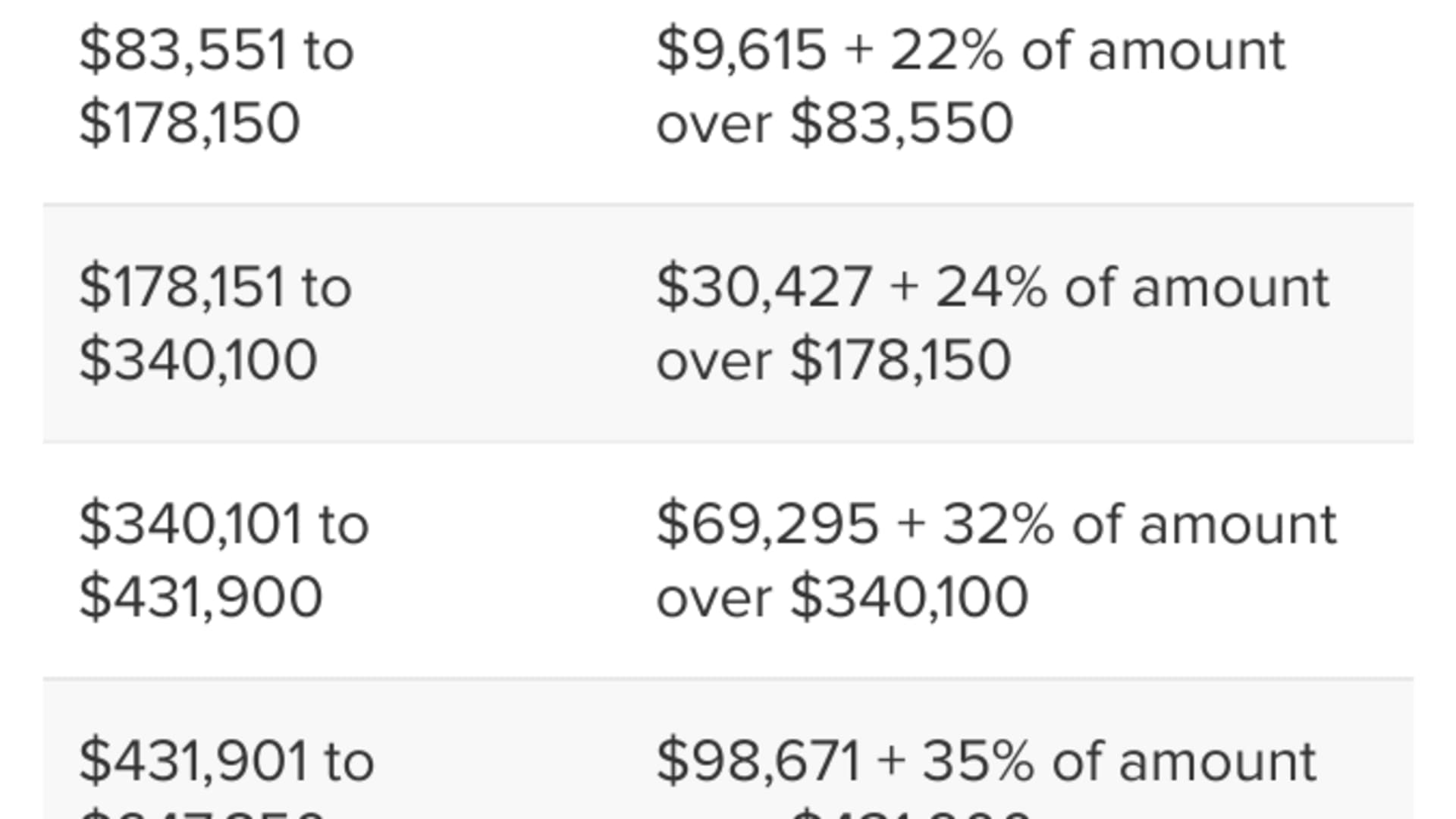

Generally, muni bonds may pay off if you're in the 32% bracket or higher, depending on state taxes, Mullikin said.

While muni bonds may pay less than a corporate bond with a similar credit rating, you have to compare each asset's after-tax yield for an apples-to-apples comparison.

For example, let's say you're in the 35% tax bracket, comparing an 8% corporate bond to a 5.25% muni bond. While 8% may seem like a higher return, you only receive 5.2% after federal taxes.

The downsides of muni bonds

While muni bonds may offer security and tax-free income, these assets may not work if you're seeking higher returns.

"Do not get into muni bonds thinking you're going to get growth," Benold said.

If you're investing long-term, experts suggest purchasing funds over individual muni bonds because it may offer more diversification.

And it can be difficult for do-it-yourself investors to monitor each muni bond for credit changes or interest rate shifts.

Moreover, when interest rates drop, there's a risk of issuers paying off their debt early to "call" the bond, and resell it with lower yields. When this happens, you lose a higher payout.

When in doubt, you may opt for professional advice to build a muni bond allocation based on your risk tolerance, timeline and goals.

"Bonds are supposed to be the safe part of a portfolio," Mullikin added. "So you really don't want to make a mistake."