People look at vehicles at AutoNation Toyota dealership in Cerritos, California.

- Consumer prices rose sharply in May, with the CPI jumping 5%, more than economists expected.

- Stocks rose and bond yields fluctuated after market pros decided the hot inflation report wouldn't lead to any changes in the Fed's easy policy.

- Economists said there are signs that rising prices could be temporary since they are centered in areas impacted by the pandemic.

Consumer prices jumped more than expected in May, but the surge in inflation looks to be temporary and should not push the Federal Reserve to tighten policy for now.

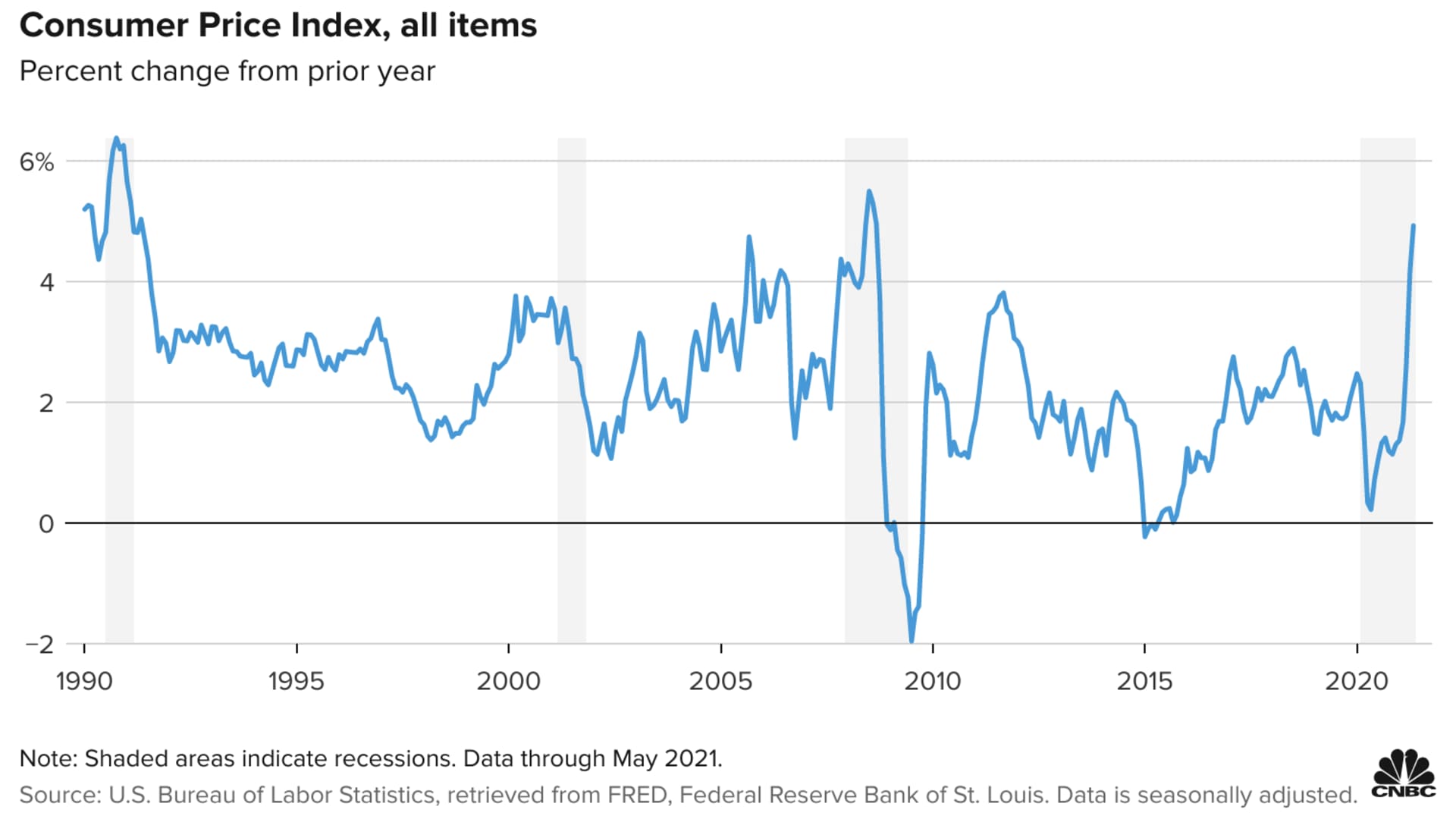

The consumer price index rose 5% in May on a year-over-year basis, the highest since the summer of 2008, when oil prices were skyrocketing. Excluding food and energy, core CPI rose 3.8% year over year, the highest pace since 1992. A third of the increase was attributed to a sharp 7.3% increase in used car and truck prices.

Get top local stories in Southern California delivered to you every morning. >Sign up for NBC LA's News Headlines newsletter.

Fed officials have described the current period of high inflation as transitory, meaning it should be brief or short-lived. They have expected several months of elevated price increases because of pent-up demand and supply chain lags. The comparison to last year's weak levels — at a time when the economy was mostly shut down — is also a factor.

"The pick-up in inflation is stronger than expected, but it still looks like it is in transitory categories," said John Briggs of NatWest Markets. "[Fed officials] can probably get away with talking about transitory."

The Federal Reserve meets June 15 and 16. There was some market speculation that if inflation looked very hot, the central bank might move up the time frame in which it would discuss moving away from its easy policies.

Money Report

Economists expect the first step toward easing would be when the Fed publicly discusses its decision to cut back on the $120 billion in Treasury and mortgage securities it buys each month.

The bond buying, or so-called "quantitative easing" program, was designed to create liquidity and keep interest rates low.

After starting the discussion about its bond program, the central bank is then expected to wait several months before beginning a gradual whittling away of purchases until it gets to zero. The Fed would then consider raising its target federal fund rate from zero, but that is not expected until 2023.

Many economists have been expecting the Fed to first talk about tapering bond buying at its Jackson Hole Economic Symposium in late August, before actually cutting the size of purchases in late 2021 or next year.

Mark Zandi, chief economist at Moody's Analytics, said there's evidence the price pressures could be fleeting, as the Fed expects.

"A lot of the surge in prices are for things that are just normalizing. ... Hotels and rental cars and used vehicles, sporting events, restaurants. Everyone is just getting back to normal, so pricing is just returning to what it was pre-pandemic," Zandi said.

However, he added that it's too soon to say inflation won't be more persistent than the Fed expects. "It's premature to conclude all of this is transitory and where underlying inflation is ultimately going to land when we get through the price normalizations," Zandi said. He expects when the surge is over, inflation will be at a higher level than it was pre-pandemic.

The Fed has said it would tolerate inflation running above its 2% target, and it would consider an average range for those price increases. That means it has committed to hold off on raising interest rates as soon as it sees inflation risks rising, as it has done in the past.

Financial markets took the surge in CPI in stride, and stocks jumped after the 8:30 a.m. ET report. The Dow gained more than 200 points but gave up its best gains. The 10-year Treasury was slightly higher at 1.49%, after initially rising as high as 1.53%. Yields move opposite price. Fears the inflation number would push the Fed to shift policy sooner would have driven yields much higher.

The components of higher prices

Economists said some of the price increases were surprising, but the price gains in the bigger contributors to CPI remained relatively subdued.

"The used car component is just stunning," said Grant Thornton chief economist Diane Swonk. "What's kind of surprising is how low the shelter component has remained. It's coming up from where it decelerated. There's now the question of it picking up. We have to watch that, but I would have expected more of a hotel room increase in shelter."

Shelter accounts for more than 30% of CPI. The shelter index rose 0.3% in May, and 2.2% over the last 12 months. The rent portion rose 0.2%, and the index for owners' equivalent rent — or the hypothetical amount a homeowner would charge someone to rent their dwelling — rose 0.3%. Lodging away from home rose just 0.4%, after jumping 7.6% in April.

Another big component, medical care, fell 0.1% after rising in the four previous months. Medical care prices rose just 0.9% over the past 12 months, the smallest increase since the period ending March 1941.

"Medical care and housing are two very large components of inflation. They're both very sticky and a reason to think inflation will settle at a higher level but not at a level that is uncomfortable," said Zandi. "The reason for being so sanguine is around medical care and housing." He said the expansion of the Affordable Care Act has helped hold down medical costs.

Grant Thornton's Swonk said she does not expect much from the Fed next week and the inflation report does not change that.

"The remarkable resilience of the long bond — it gives the Fed the opportunity to think about tapering, because financial markets are buying it as a transitory surge in inflation," Swonk said, referring to the 30-year Treasury.

Investors have been buying the 10-year and 30-year Treasury bonds since last week's weaker-than-expected May jobs report. The 30-year yield has fallen to 2.16%. Bond yields move opposite prices.

For now, investors are not fearful the Fed will move sooner, but Swonk says there could still be a few more hot inflation reports.

"It's higher than [Fed officials] would like. It surprised to the upside. My guess is it lasts longer than they expect. I expect it to last longer and be hotter but still go away," she said.

But she still expects the Fed to wait until the end of the summer to talk about changing its bond purchases.

"I always expected tapering talk to begin more openly at the Jackson Hole meeting. It hasn't changed my view. Some people thought the Fed would get closer to full employment before they did liftoff on tapering," Swonk said.

She said some data in the CPI report dovetails with the jobs data. The economy created 559,000 jobs in May, about 100,000 less than expected.

"If you look at the combination of events — used car prices, insurance costs on vehicles, all of these things accelerated and now they're rebounding. Prices at the pump, they're up over 50% from a year ago," Swonk said. "All of this is making it harder for workers to get to low-wage jobs."