Why Layoffs and the Job Market May Not Repeat Recession History in This Economy

- The layoffs that have made the headlines recently, from Stripe to Twitter, are concentrated in sectors of the economy most-sensitive to interest rates, such as housing and autos, and where companies "over-hired," predominantly in technology.

- Several demographic factors, from baby boomer retirements to a declining working age population and persistently low labor force participation rate, are reasons employers may be less likely to pull the trigger on layoffs.

- But the balance is going to shift and the leverage employees have had will be lower in a recession, and now may be the last, best chance for restless job seekers to make a move before it's too late.

The term "labor hoarding" has recently come into play within economic circles as the job market remains strong despite the Fed's best efforts to cool it down.

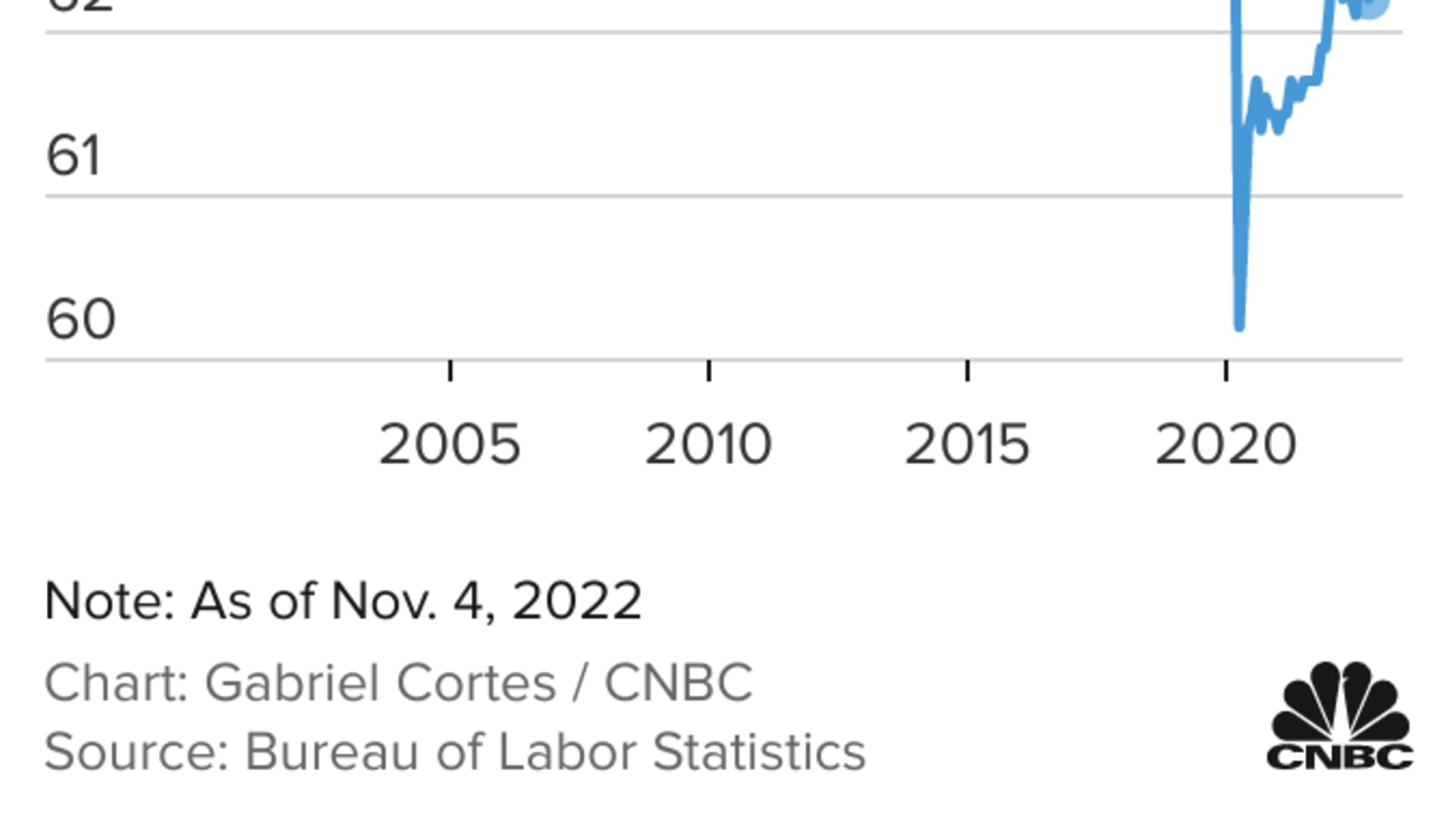

The latest jobs report shows labor market growth remaining strong, with U.S. payrolls surging by 261,000 in October, though there was a slight uptick in unemployment to 3.7%.

Even though layoffs are making the headlines, from Twitter to Stripe, the labor market is far from rolling over.

Get top local stories in Southern California delivered to you every morning. >Sign up for NBC LA's News Headlines newsletter.

"There have been several thousand high-profile layoffs in the tech sector in the past couple of weeks. While this is unfortunate, it is useful to keep in mind that the labor market is significantly larger and has been overall healthy," Bledi Taska, chief economist at labor market consulting and research firm Lightcast, said in an email.

There are 159 million people currently employed in the US, and in the past month there were 1.3 million layoffs.

"This is fairly normal and is historically low at a layoff rate of 0.9%," he said.

Money Report

Taska noted that even in tech and at private VC-funded companies like Stripe, layoffs are not surging overall. In the Professional and Business Sector (where most of the tech companies belong) layoffs dropped in September and startup layoffs have also dropped over the past few months. "Overall this means that while it is important to follow some of the high profile tech layoffs, they are not indicative of the overall trends in the labor market, or even in the tech sector," Taska said.

Labor hoarding has become a thing given how hard it has been to find workers to fill open positions. Taska is hesitant to read too much into the talk of labor hoarding yet, and he says there's no denying the basics of labor economics in a downturn.

"You can't have as many people around if demand decreases," Taska said. "Yes, it was a period during which it has been hard to find people, but companies want people because they need them to be productive, and if people are costing too much, the bottom line will be the most important. You don't want people for the sake of people," he added.

Still, Taska and other labor market experts say the way CEOs and CFOs think about layoffs in a slower economy may be due for a change, as demographic trends that will persist beyond a single economic cycle make companies more strategic in workforce reduction planning.

Fill open positions, but maybe less of them

One primary reason labor decisions may be different than they've been in the recent past is related to all of those millions of unfilled positions, seven million before Covid which went up recently to as high as 11 million.

"At the very least, if you had 30 positions open, fill 15 of them," Taska said.

C-suites are all expecting some form of recession. A recent survey from the Conference Board and Business Council found 98% of CEOs anticipating a recession over the next 12 to 18 months.

But so far, consumer demand has held up, making it harder to move quickly to cut jobs. Bank of America CEO Brian Moynihan says continued strength is his current view of the consumer.

The recent numbers on open positions show the unpredictability related to the pace of the labor market growth.

Job openings appeared to be disappearing, with the August total a little over 10 million, a 10% drop from the over 11 million reported in July —and one million less than expected. That led to belief that "the worst of the tight labor market is over" but at 10 million-plus open jobs it is still a very healthy labor market. And that was followed by a surprise JOLTS report earlier this week showing an increase in open positions at a time when economists have been expecting a lower number.

While the headlines focus on the job cuts and hiring freezes that have been announced, those are concentrated in sectors with the most sensitivity to Federal Reserve policy, and the Fed keeps raising rates. Even though there were hints at this week's FOMC meeting it might consider slowing the pace, the commentary from Fed Chair Powell was far from clear on future policy being more dovish. So far, the labor market slowdown story is mostly tech, where hiring was overly aggressive — Microsoft recently announced another round of layoffs and Amazon announced a corporate hiring freeze.

Most firms don't want to "overshoot" on people in either direction.

"Firing people is no fun, but you don't want to over-hire," Taska said. "Let's start with revising the outlook on open positions versus where it was three to four months ago. This is not the phase for 'fire first' except in tech, where they over-hired," he said.

Labor participation remains low

The number of people working or looking for work remains near historical lows as measured by the labor force participation rate and it has been in a downward trend for a decade. That means for now, and in a recession that turns out to be less than severe, employers may be able to adjust for the gap in the labor market by simply not posting new jobs for a period of time.

While the labor market typically lags the economy, layoffs would have been expected to pick up already.

"We see almost no signs of mass layoffs other than in the areas most sensitive to interest rates," said Andrew Challenger, senior v.p. at Challenger, Gray & Christmas, which works with firms to help transition employees out of their workforces. "We're seeing a slight uptick in tech and auto and construction."

"When I talk to HR they are still in full-on hiring model," he said. "They've just been in hiring mode for a long time and just all hands on deck in trying to get people into the organization, trying to deal with quit rates they've never seen before and massive turnover in roles."

That could change. In fact, Challenger thinks the labor lag effect will be a factor in 2023, but he is less than confident in making that call. "Three to six months from now I think it will be different, but I also thought that six months ago," he said.

Keep the bigger demographic picture in focus

The biggest driver of labor market tightness was, and will remain, the aging population and baby boomers retiring. This is one reason why it remains better to align supply to demand as far as total number of job openings rather than look to layoffs, says Lightcast senior economist Elizabeth Crofoot.

By 2025, the number of high school graduates is expected to peak and after that, it will be in decline during a period of time when retirements are accelerating.

"In a year and a half, we will see even fewer and fewer people available to take jobs. These forces will just accelerate through 2030, so the next several years it will be harder and harder to find people," Crofoot says.

The U.S. has also failed to pass any bipartisan immigration reform which would create a foreign talent pool that many business leaders say will be needed to fill jobs into the future. U.S. Secretary of Labor Marty Walsh recently told CNBC the lack of immigration reform will be a "catastrophe" for the economy.

Don't expect people to be waiting for jobs

The 2008 recession led to a "jobless recovery." Don't expect that to happen again.

"This will be a very distinct recession where people may still have jobs," Crofoot said.

She notes that the unemployment level that the Fed is targeting (4.4% by 2023) is not high by historical standards.

After 2008, it took the employment market roughly three years to catch up to the economic rebound.

This time, "the talent pool will be much smaller than you would expect after a recession," she says. "I think there will be some give and take from employers, and they will tread more carefully. Otherwise, they will have a very hard time replacing people. There won't be a huge horde waiting for jobs."

Get your next job now

The current labor market remains challenging to forecast, as many businesses plan for a recession but don't see the weakness in consumer demand occurring rapidly enough to support a large workforce reduction.

Companies that over-hired needing to move to a more conservative stance on costs on the expectation of slower growth isn't the same kind of labor market negative as a Covid, "when the knife is falling and employers are scared about their own lives," Challenger said. "Those are different situations. This is not panic," he said.

At the same time, the longer-term demographic factors and increased cost of recruiting and training new workers is a reason to move more "strategically" Crofoot said, when it comes to workforce reductions.

But even with the labor market numbers remaining strong, now may be the last "best" time to get a new job for those seeking a move. There is the risk that the Fed overshoots on its interest rate increases and a job market that has remained strong will see a dramatic decrease in a severe recession, and more rapidly than expected by the central bank, with unemployment rising higher than its target. And even if that worst-case scenario doesn't come to pass, "Employers will get antsy and stop offering higher pay and benefits," Crofoot said. "Worker leverage will decrease, and won't be able to demand those higher pay levels, or hiring bonuses. So this is the time to be making a move. Make it now," she said.

The one move not to make

Along with labor hoarding there has been a lot of talking about "quiet quitting." Some firms may be betting that they will be able to avoid layoffs through return-to-office mandates and some recent data indicates offers of remote work going down. Employees who don't want to come back will end up leaving the organization. Elon Musk demonstrated this CEO mentality earlier this year when he said workers should come back minimum 40 hours a week or quit.

This thinking remains on the margins, but it is a concern within companies. Challenger said his surveying of HR leaders shows that 10% worry their C-suites will look to this source of attrition in headcount. According to labor experts, while Elon Musk has many good ideas, this is not one of them.

Indiscriminate job losses are not the way to go unless firms want to risk losing some of their most high-value employees, especially those able to command good positions from firms still hiring remotely. The permanent remote workforce has more than tripled since 2019 to near 18% of the labor market.

Any firm considering layoffs should start by evaluating the workers that have been the most productive, and those who have not, and from that evaluation figure out whom to let go.

"I wouldn't be surprised if there are some internal discussions around this angle, but employers risk losing their best talent," Crofoot says. In fact, she adds that this idea really runs counter to everything C-suites should have learned about the labor market in the past decade.

"I don't think employers have that wiggle room when we are talking about an overall labor supply that is dwindling. There has to be some recognition of the value of employees and not treating them as dispensable."